Coronavirus Outbreak Intensifies

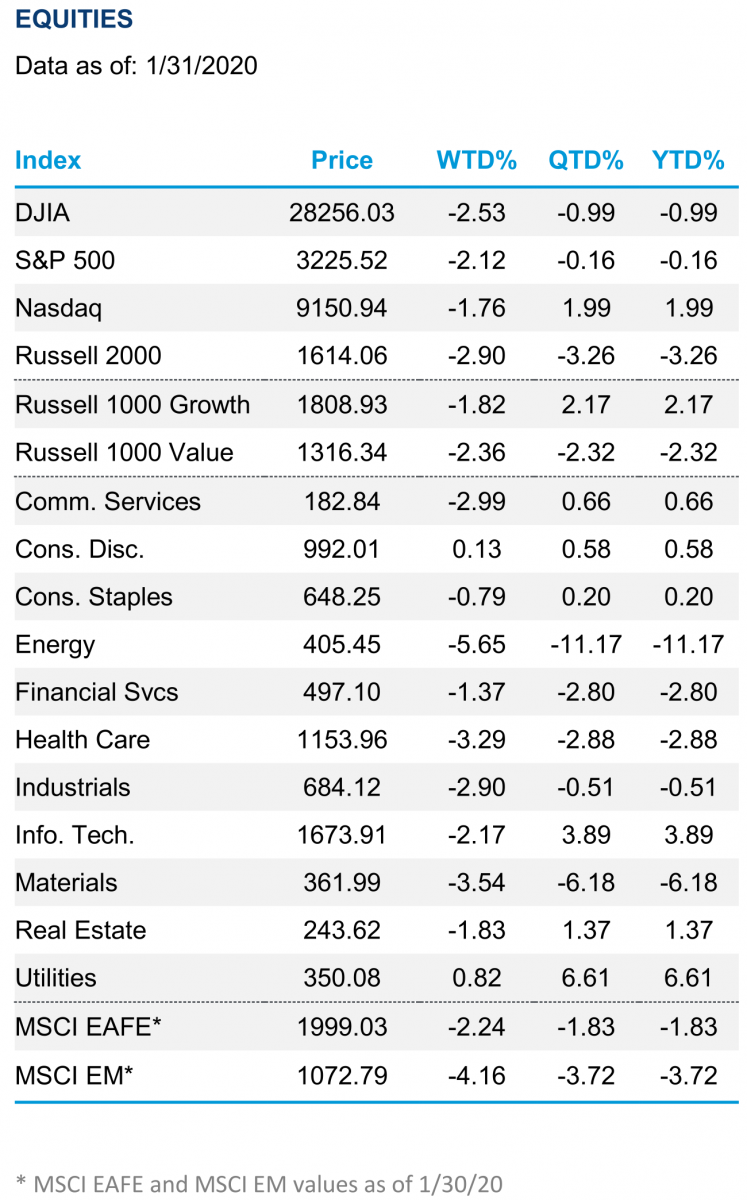

U.S. stocks fell for the second straight week, as the S&P 500 Index slid more than 2% as the coronavirus outbreak spread rapidly within China and fears of a global outbreak increased. Good earnings results overall, particularly for tech and internet retail companies, helped offset some of the hit to investor sentiment.

All four U.S. indexes we track fell during the week, with the Nasdaq Composite falling less thanks to earnings-driven gains in the consumer discretionary sector. The small cap Russell 2000 Index underperformed the S&P 500, while growth stocks, buoyed by Amazon, held up better than their counterparts on the value side, which was weighed down by energy sector losses.

This week’s economic calendar featured U.S. gross domestic product (GDP), which rose 2.1% in the fourth quarter of 2019, slightly above Bloomberg’s 2% consensus forecast. Net exports added 1.5 percentage points, its largest contribution to quarterly GDP growth in 10 years, as global demand picked up and domestic demand slumped. The Federal Reserve held rates unchanged, as expected, but it did slightly downgrade its consumer outlook, even as the Conference Board’s consumer confidence index improved solidly in January.

Global stocks lagged the United States through Thursday’s close. The MSCI Emerging Markets (EM) Index fell more than 4% through Thursday as the number of coronavirus cases in China increased and business and travel restrictions tightened. MSCI’s index of developed-market stocks also lagged, amid the slowest euro-area GDP growth (0.1%) in nearly seven years. Market weakness was concentrated in Hong Kong, Japan, and Germany.

Fixed Income, Currencies, and Commodities

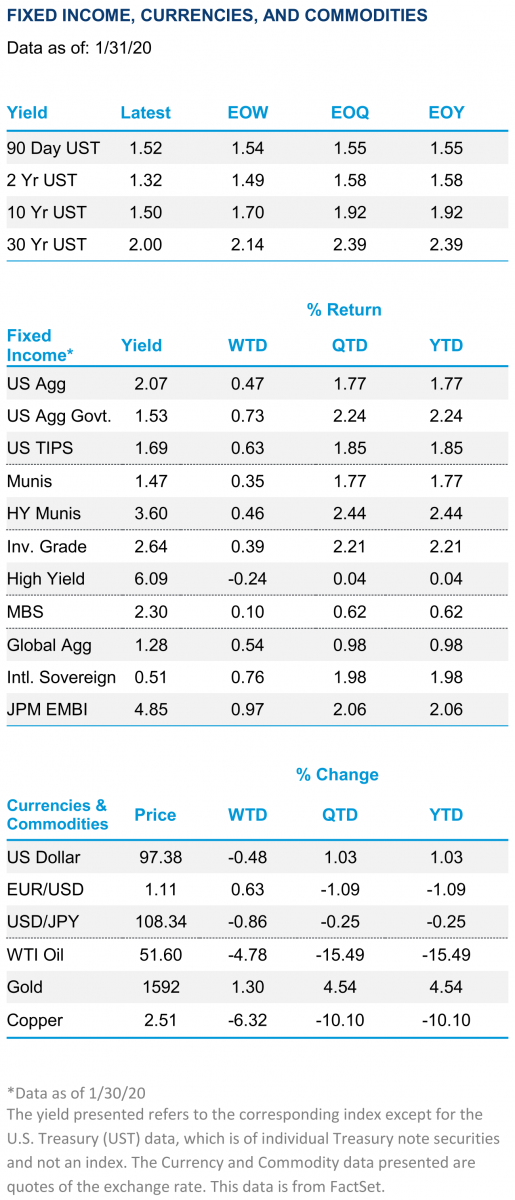

Fixed income prices benefited from a continued rush to safe-haven assets. The 10-year U.S. Treasury yield dropped sharply, shedding 20 basis points (0.2%), flattening the yield curve considerably, and causing the 3-month/10-year yield spread to end the week in inversion territory. The Bloomberg Barclays U.S. Aggregate Bond Index climbed 0.47% through Thursday. Emerging market bonds and international sovereign debt led returns during the week, while high-yield corporate bonds posted a negative return.

The U.S. dollar suffered its first weekly loss in the past four weeks as the flight-to-safety boost that bonds received didn’t carry over to currencies. Gold did get a lift from market participants looking for safety. Lower interest rates also tended to help gold prices, all else equal. Copper and oil both fell sharply amid fears of lower demand from China due to the coronavirus outbreak.

The economic calendar will bring several key reports as the calendar turns to February. On Monday and Wednesday, investors will get the January Institute for Supply Management (ISM) Purchasing Managers’ Index (PMI) for manufacturing and services. Preliminary labor cost and productivity data for the fourth quarter of 2019 will be reported on Thursday. Friday will bring the widely followed payroll employment report for January (Bloomberg consensus is 156,000 jobs created). Earnings season continues with 94 S&P 500 companies slated to report quarterly results.

Internationally, investors will get a heavy dose of European data, including Markit’s manufacturing PMI data for Germany and the broad Eurozone on Monday; Eurozone wholesale inflation on Tuesday; retail sales on Wednesday; and German factory orders, trade, and industrial production data on Thursday and Friday.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance the products or strategies discussed are suitable for all investors or will yield positive outcomes. All performance referenced is historical and is no guarantee of future results. The economic forecasts set may not develop as predicted.

- All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Sector data is represented by S&P 500 GICS sub-indexes.

- Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

- Investing in gold is subject to risks including loss of value. The price swings in commodities and currencies can result in significant volatility in an investor’s holdings.

- U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

- All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

- For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

- This research material has been prepared by LPL Financial LLC.

- Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisorthat is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- If your advisor is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

- Tracking # 1-945698

Contact us directly should you have questions about this topic.