2.5.25 Why Not Both? Blending Active and Passive Management

Reframing the Active-Passive Debate

There is much debate on whether active investment managers can consistently outperform passive benchmark indexes, often framed as “active versus passive.” When framed this way, the word “versus” implies there is stark opposition between the two concepts or that perhaps they are irreconcilable. Our view is different, as we believe it can be beneficial to use active and passive management together in portfolios.

Active managers choose stocks, bonds, or other securities based on their research and outlook, often attempting to outperform a benchmark index. Meanwhile, passive managers attempt to replicate the performance of a benchmark index, often with lower costs and less portfolio turnover. While focused on index-like exposure, passive investing may reduce key-person risk and style drift, which may occur when active managers venture away from the exposure the investor wanted.

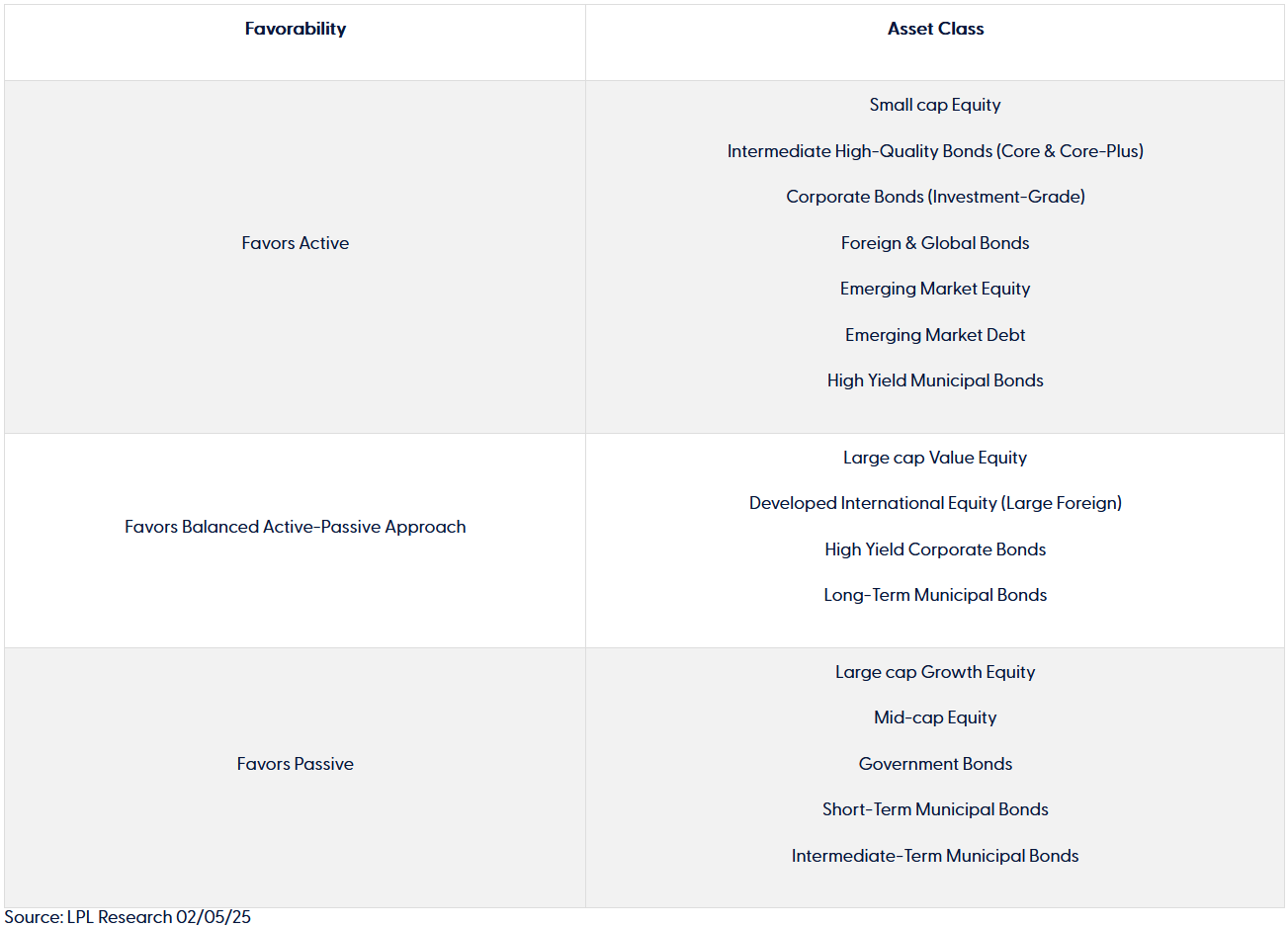

LPL Research created a framework that allows our Active-Passive portfolios to tilt toward active management in the asset classes where our research suggests it may have greater potential for outperformance. Weighted-average expenses for the overall portfolio may be controlled by paying for active management only where we believe it is likely to succeed. The “Best of Both Worlds” table summarizes how a blended Active-Passive portfolio may combine the benefits of active and passive management.

Best of Both Worlds?

Framework Methods

Our study of active management began with a quantitative (hard data) analysis of historical risks and returns. We grouped actively managed mutual funds into asset classes based on the benchmarks listed in their prospectus documents. The study included over 4,200 stock funds and over 1,700 bond funds, using up to 20 years of historical data. The criteria used to assess active management included 10 different measures across four categories:

• Average over- or under-performance (excess return) of funds compared to their benchmark indexes. Conceptually, this is similar to investing $1 in each fund within a certain asset class. To deem active management favorable on this measure, we generally wanted positive excess returns.

• Percentage of funds that outperformed their benchmark indexes. This can be thought of as the probability of picking a fund that outperformed if an investor randomly picked one fund within a certain asset class. We generally wanted over 50% of the active funds to outperform, measured over various three-year periods within the last 20 years.

• Risk-adjusted performance, as measured by information ratio. A fund’s information ratio is its excess return divided by its tracking error, which measures volatility relative to the benchmark index. When the information ratios were higher, we generally had a more favorable opinion of active management.

• The excess returns of top-performing funds (top 25% versus benchmark) and the excess returns of bottom-performing funds (bottom 25% versus benchmark). This measured the size of the reward for choosing funds wisely and the penalty if fund selection is ineffective. We generally wanted this ratio to be above one.

Importantly, we evaluated the actual costs of passive management, because it is not free and varies across funds and across asset classes. We also considered that, in some asset classes, it may be more difficult for passive managers to closely replicate the returns of the benchmark index. Finally, we considered softer “qualitative” criteria that may impact the success of active management, such as benchmark concentrations or unique risks that are hard to quantify.

Framework Output

Applying our framework, asset classes were placed into one of three buckets: Favors Active, Favors Passive, or Favors a Balanced Active-Passive Approach. We relied heavily on our quantitative (hard data) analysis when making these placements. In a select few cases where the quantitative data did not capture unique risks or challenges, we made a qualitative adjustment to the asset class placement. For example, we took a more favorable view of active management within emerging market (EM) equity than would be indicated purely by the hard data. In EM, where geopolitical risks may be frequent and severe, we believe active management may often be preferable to passive investments forced to invest in certain countries or sectors due to benchmark construction.

Asset Class Placements

While data analysis, rather than preconceptions, guided our asset class placements, it is interesting to consider common traits among the asset classes in the Favors Active bucket. Many of the asset classes that have been favorable to active management have a wide range of securities in their investable universe, which may allow active managers a broader opportunity set. In small cap, for example, there are more companies available for active managers to scour for opportunities, as compared to mid-cap and large cap. Core- and core-plus and foreign and global bond funds may benefit from the many varied decisions active managers are able to make, such as which sectors and maturities to emphasize, in addition to security selection. In contrast, the decisions available to government bond managers are somewhat limited, as one government bond may differ from another only in its maturity date, which may limit the potential for differentiated returns.

Key Points

We find benefits to blending active and passive management. By emphasizing active management in asset classes where it may be more likely to succeed, portfolio expenses may be reduced while retaining performance potential. Our quantitative analysis over the last 20 years suggests that active management has often been successful within small cap equities, core- and core-plus bonds, and foreign and global bonds, all of which are grouped in the Favors Active bucket. In some asset classes, such as large cap value equities and developed international equities, active management delivered occasional or modest benefits that may be roughly in balance with the benefits of passive management. In large cap growth equities, mid-cap equities, and government bonds, even the best active managers often struggle to outperform passively managed investments. While they are placed in the Favors Passive bucket, there may still be instances when certain active managers are appropriate for Active-Passive portfolios. Our rigorous framework for evaluating active management is one of many inputs LPL Research considers when managing its Active-Passive portfolios. We believe the LPL Research Tactical Active-Passive model portfolios may allow investors to benefit from active management and low-cost passive investing while adhering to LPL Research’s rigorous asset allocation, investment manager research, portfolio construction, and risk management principles.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #692556