Midyear Outlook 2026

Policy, Buildouts, and Bottlenecks

2026 Midyear Market Outlook

Markets are expected to remain influenced by policy decisions, artificial intelligence investment, interest-rate expectations, election uncertainty, and global resource security.

Use the contents below to jump directly to each section. The anchor links have been adjusted so section titles are not hidden behind the website’s fixed header.

Contents

Growth is expected to moderate but remain positive,

supported by business investment and consumer balance sheet strength.

Equity markets may continue to benefit from earnings growth, though selectivity and diversification remain important.

Income remains an important driver as Treasury yields are expected to stay range-bound in a higher-for-longer environment.

A balanced allocation may help investors navigate policy shifts, AI uncertainty, and geopolitical volatility.

Four Key Themes to Watch

The market outlook is shaped by four central themes: U.S. midterm elections, rising resource nationalism, artificial intelligence moving from buildout to return on investment, and a Federal Reserve leadership transition amid elevated inflation and geopolitical uncertainty.

Policy and elections

Midterm elections may influence regulatory priorities, fiscal debates, and investor sentiment. Policy uncertainty can create volatility, but it can also create opportunities for disciplined investors.

Innovation and execution

Artificial intelligence remains a powerful theme, but market attention is moving from enthusiasm about infrastructure spending toward evidence of practical returns and profitability.

Midterm Elections

With midterm elections approaching, markets may react to possible shifts in congressional control, budget negotiations, the debt ceiling, regulation, and tax policy. A split Congress may limit the likelihood of large legislative changes, but it can also increase the chance of policy standoffs.

Election years can bring short-term uncertainty. For long-term investors, the important point is to avoid letting campaign headlines drive emotional decisions and instead keep attention on fundamentals, risk tolerance, and overall portfolio positioning.

Planning consideration: Volatility around elections is normal. Review risk exposure, confirm liquidity needs, and keep a diversified allocation aligned with long-term goals.

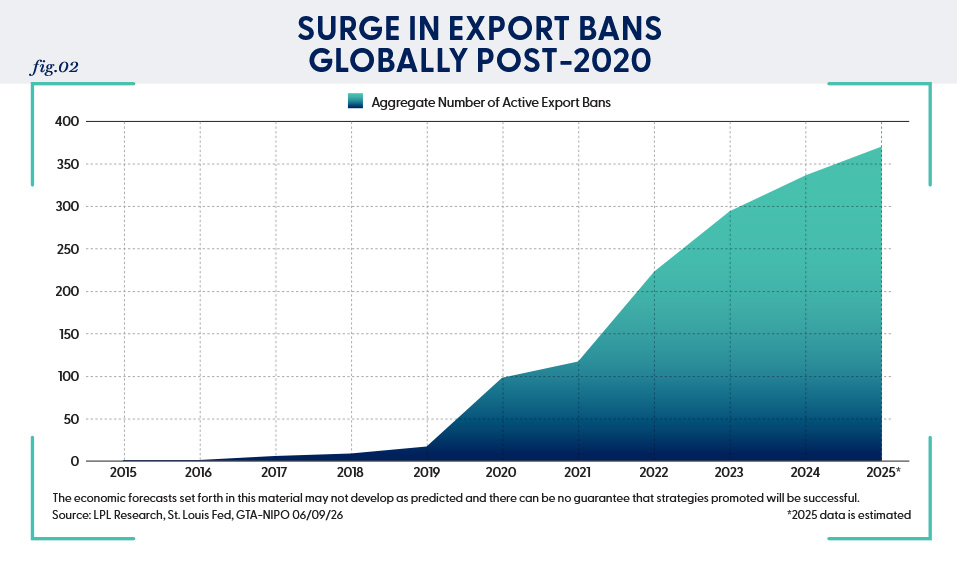

Resource Nationalism

Resource nationalism reflects the growing desire of governments to secure access to energy, metals, food, and strategic materials. This trend can affect supply chains, trade relationships, inflation pressures, and the investment outlook for commodity-linked sectors.

As countries place greater emphasis on control and security of natural resources, investors may see renewed interest in real assets, energy, materials, infrastructure, and regions tied to commodity production.

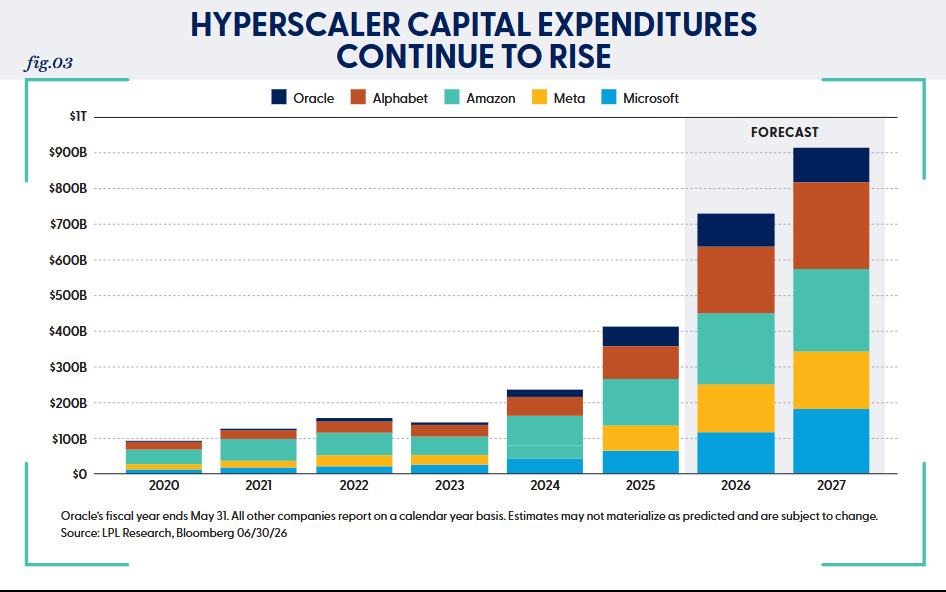

Artificial Intelligence: From Buildout to Returns

Artificial intelligence continues to influence capital spending, productivity, earnings expectations, and market leadership. The next phase may be more selective, with investors focusing on which companies can convert AI investment into measurable business results.

Infrastructure spending remains substantial, but the market may increasingly scrutinize return on investment. Companies that can use AI to improve margins, increase productivity, or strengthen competitive advantages may be better positioned than companies relying only on the broader AI narrative.

Planning consideration: AI remains important, but concentration risk should be monitored. Diversification may help investors participate in innovation while reducing dependence on a narrow group of companies.

Monetary Policy and Interest Rates

Inflation, energy prices, wage trends, and geopolitical events are expected to keep monetary policy in focus. A prolonged pause in rate cuts may leave Treasury yields range-bound, with income playing an important role in bond returns.

Investors should be prepared for rate expectations to change as new data becomes available. A patient approach may be appropriate while the Federal Reserve balances inflation control with economic stability.

Economy

Economic growth is expected to moderate but remain positive. Strong business investment, including spending tied to artificial intelligence, intellectual property, productivity, and non-residential structures, may help offset weakness in housing and other interest-rate-sensitive sectors.

Consumer demand may remain supported by household wealth, though inflation and borrowing costs can still pressure spending. Unemployment may edge higher but is expected to remain historically low if the economy continues to avoid recession.

- Business investment remains a key source of support.

- Housing continues to face pressure from higher borrowing costs.

- Inflation may ease if geopolitical pressures and energy costs moderate.

- Labor market conditions may soften without necessarily signaling recession.

Stocks

Stocks may continue to benefit from an improving but still challenging macro backdrop, strong earnings growth, and AI-related investment. However, market gains may become more selective as investors evaluate valuations, profit margins, and the durability of technology-led leadership.

Diversification remains important because leadership can rotate. A balanced equity approach can help investors participate in long-term growth while reducing reliance on a single theme or sector.

Sector Recommendations

Sector leadership may shift as policy, interest rates, earnings, energy prices, and AI investment expectations change. Technology remains central to the market narrative, but the strongest performers may need to demonstrate real earnings benefits and disciplined capital allocation.

Areas connected to infrastructure, energy security, productivity, and high-quality defensive characteristics may deserve attention as investors weigh both opportunity and volatility.

Bonds

Bond returns may be driven primarily by income while Treasury yields remain range-bound. A higher-for-longer interest rate environment can make high-quality bond allocations useful for portfolio stability and cash-flow planning.

Credit spreads may remain contained if corporate fundamentals stay resilient, but investors should continue to focus on quality, duration, and the role bonds play within the broader portfolio.

Alternative Investments

Alternative investments may help enhance portfolio resilience when markets are influenced by policy uncertainty, geopolitical shocks, interest-rate changes, and stock-level dispersion. Strategies such as infrastructure, private credit, market neutral, managed futures, and global macro may play a role for appropriate investors.

Because alternatives can involve complexity, liquidity limitations, and unique risks, they should be evaluated carefully within the context of each investor’s objectives and risk tolerance.

Commodities and Currency

Commodities and currency markets may remain sensitive to geopolitical risk, resource security, export restrictions, energy supply, central bank policy, and the direction of the U.S. dollar. Resource nationalism may support interest in commodity-linked sectors and regions.

These areas can be volatile, but they may also provide diversification benefits when inflation, supply constraints, or geopolitical tensions affect traditional stock and bond markets.

Tactical Views

Tactical positioning may favor selectivity, quality, diversification, and balance. U.S. equities may remain supported by resilient growth and AI innovation, while value, minimum volatility, and select international or commodity-linked exposures may help broaden portfolio opportunity.

Investors should remain flexible. The path of inflation, interest rates, energy prices, AI monetization, and election outcomes may influence market leadership as the year unfolds.

Summary

The 2026 midyear outlook suggests a market environment that is constructive but not without risk. Economic growth may remain positive, AI continues to reshape investment and earnings expectations, interest rates may stay higher for longer, and policy developments may create periods of volatility.

For investors, the key is not to predict every market turn. The priority is to remain disciplined, diversified, and aligned with a thoughtful financial plan.

This page is for general informational purposes only and should not be considered individualized investment advice. Market forecasts may not develop as expected. All investing involves risk, including possible loss of principal.