2.25.26 Competitors to the Greenback Are Less Significant

Hypothetical Scenario

Let’s develop a scenario to explain the importance of foreign exchange (FX) markets and specifically, the dominance of the U.S. dollar. Say, for example, Thailand, one of the world’s major rice exporters, engages in trade with Brazil, the second‑largest cotton exporter. When these two countries conduct bilateral trade, they typically do not settle transactions directly in Thai baht or Brazilian real. Instead, they frequently convert their home currencies into U.S. dollars, the dominant invoicing and settlement currency in global trade and FX markets. Because the U.S. dollar is one of the most liquid and widely accepted intermediaries for cross‑border payments, it is the de facto choice for this hypothetical Thai-Brazilian trade settlement.

Dominance of the Dollar

The previous scenario explains why the dollar has maintained such dominance in global trade. One of the most convincing stats for the dollar’s reserve currency status is the fact that the U.S. dollar is in roughly 90% of all global FX transactions. And that hasn’t materially changed for over two decades. But in contrast, in recent years, the euro was in roughly 30% of FX transactions, down from roughly 40% in 2010[1].

Network effects help explain why the U.S. dollar maintains its dominant role as the world’s primary reserve currency. Because so many countries, financial institutions, and global markets already use the dollar for trade, investment, and reserve holdings, its value and convenience increase as more participants rely on it. This broad adoption creates a self‑reinforcing cycle: central banks continue to hold dollars because many global transactions are dollar‑denominated, and global transactions remain dollar‑denominated because central banks continue to hold dollars. Because so many are already using the dominant product, switching becomes difficult, and competitors struggle to gain traction.

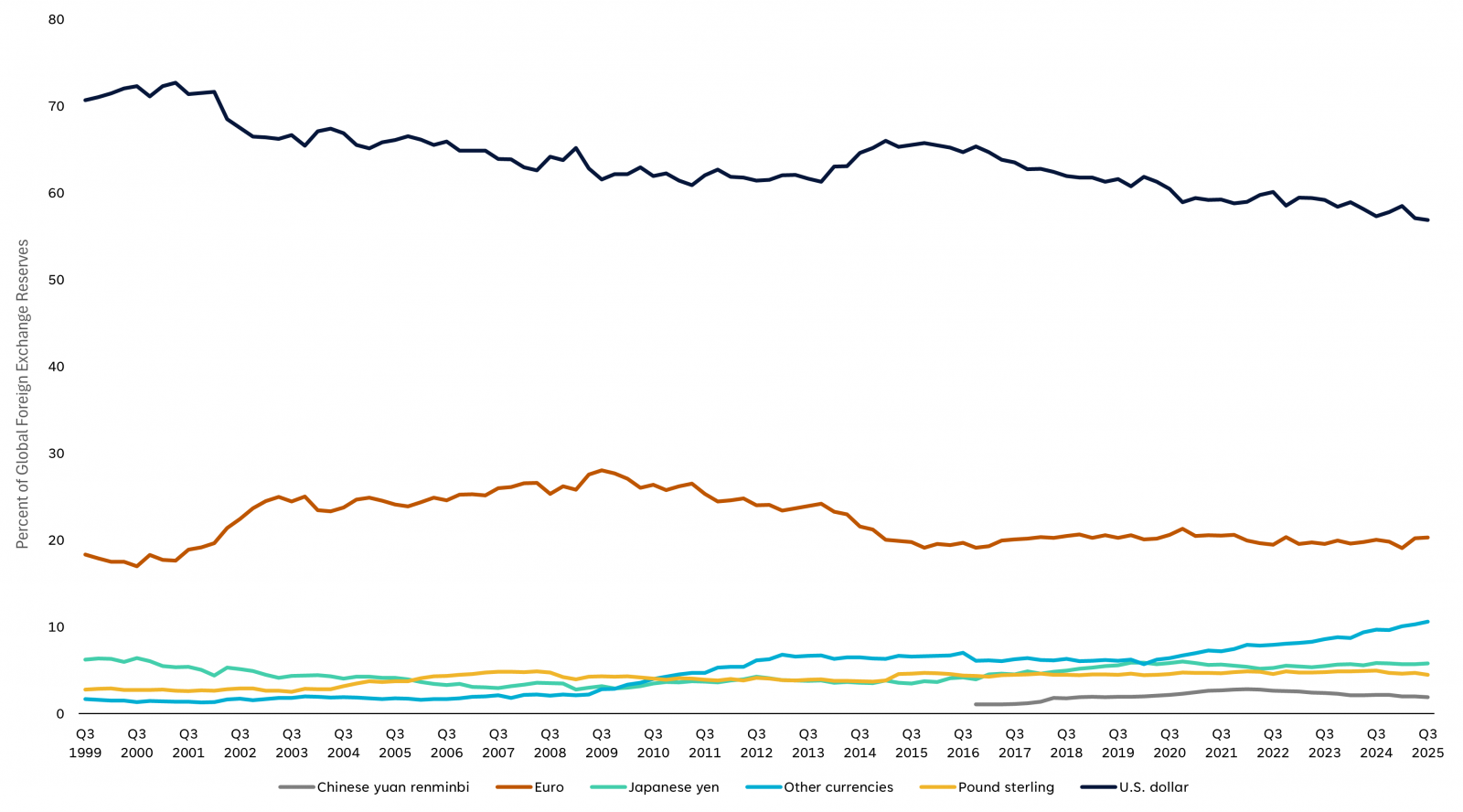

In addition to the vast majority of all FX transactions, the dollar makes up a sizable share of foreign exchange reserves. The International Monetary Fund’s Currency Composition of Official Foreign Exchange Reserves (COFER) data underscore this dynamic, showing that the U.S. dollar represents the largest share of global foreign exchange reserves. For example, it accounted for roughly 57% of world reserves in the latter half of 2025.

U.S. Dollar Has the Largest Share of Global Foreign Exchange Reserves

- Source: LPL Research, International Monetary Fund 02/25/26

But Not Without Competitors

Such persistent scale and liquidity make it difficult for alternative currencies to displace the dollar, illustrating how network effects entrench incumbency in the international monetary system.

The BRICS nations (Brazil, Russia, India, China, and South Africa, along with newly expanded members) have worked to create a network for cross‑border transactions in national currencies without relying on Western‑dominated systems like SWIFT or reserve currencies such as the U.S. dollar but have run into challenges getting other trading partners to align[2]. Nations unhappy with dollar dominance will continue to iterate on ways to displace the dollar so threats will continue. But as the Fed paper explains, the dollar is deeply embedded in global finance and will likely remain dominant “for the foreseeable future.”

Conclusion

Trading tensions could create fodder for countries to coalesce around non-dollar denominated trading. Political firestorms, such as a politicized Federal Reserve, also create stresses in cross-border payments. Over the longer term, several developments could gradually increase the appeal of alternative currencies. Geopolitical concerns have prompted discussion about diversification, but the dollar’s reserve share has not meaningfully declined, partly because most other major reserve currencies are issued by U.S. allies. Greater European fiscal integration and the expansion of jointly issued EU bonds could strengthen the euro’s role, though political fragmentation remains a limiting factor. China’s economic size continues to grow, yet the renminbi’s international prospects are constrained by capital controls, limited convertibility, and weak investor confidence. Technological shifts, including digital currencies and stablecoins, could either weaken or reinforce the dollar, especially since most stablecoins are already dollar‑linked. Overall, absent severe disruptions to dollar stability combined with major improvements in competing currencies, the dollar is likely to remain the world’s dominant reserve currency for the foreseeable future.

- [1] See Fig. 11, The Fed - The International Role of the U.S. Dollar – 2025 Edition “Because one currency is purchased and another currency is sold in FX transactions, each trade is counted twice, so the sum of the FX transactions measure is 200 percent.”

- [2] The BIS announced in October 2024 that it was handing the project over to the partners. Project mBridge reached minimum viable product stage

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #1070107

Contact us directly should you have questions about this topic.