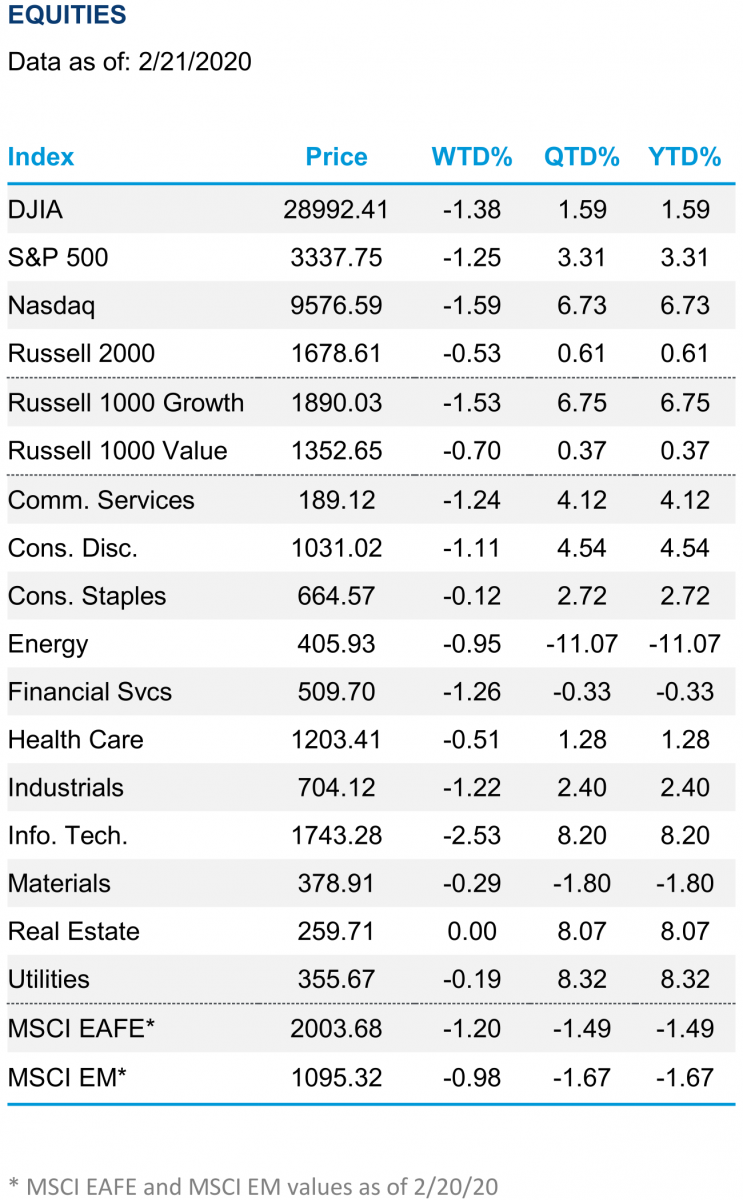

Stocks Fell as China Stayed in Focus

U.S. stocks fell during the holiday-shortened week as confirmed cases of coronavirus (COVID-19) continued to rise. The S&P 500 Index still set a fresh record high on Wednesday, partly due to China’s aggressive policy response, but pulled back Thursday and Friday to end the week lower. Earnings news from corporate America generally met expectations, while the Democratic presidential debate kept politics in focus.

The major U.S. stock indexes all ended the week lower, with the Russell 2000 Index holding up relatively well. The defensive consumer staples, real estate, and utilities sectors outperformed, while the growth-heavy technology sector fell the most and helped value stocks to outpace growth.

This week’s U.S. economic calendar featured a 0.8% jump in the Leading Economic Index (LEI) for January, the second biggest monthly change in six years. Markit’s manufacturing Purchasing Managers’ Indexes (PMI) came in below expectations, while the services PMI dropped below 50 to its lowest reading in six years. The core Producer Price Index (PPI), excluding food and energy, rose more than expected, but at 1.8% year over year, it remains contained. The week’s housing data was solid and well above expectations.

Developed international and emerging markets stocks suffered similar losses as the United States, with 1.2% and 1% declines through Thursday, based on the MSCI EAFE and MSCI Emerging Markets (EM) indexes. Weakness was concentrated in Japan, South Korea, and Taiwan, areas affected by COVID-19. The UK market bucked the trend and rose over the first four days of the week on solid retail sales and manufacturing data.

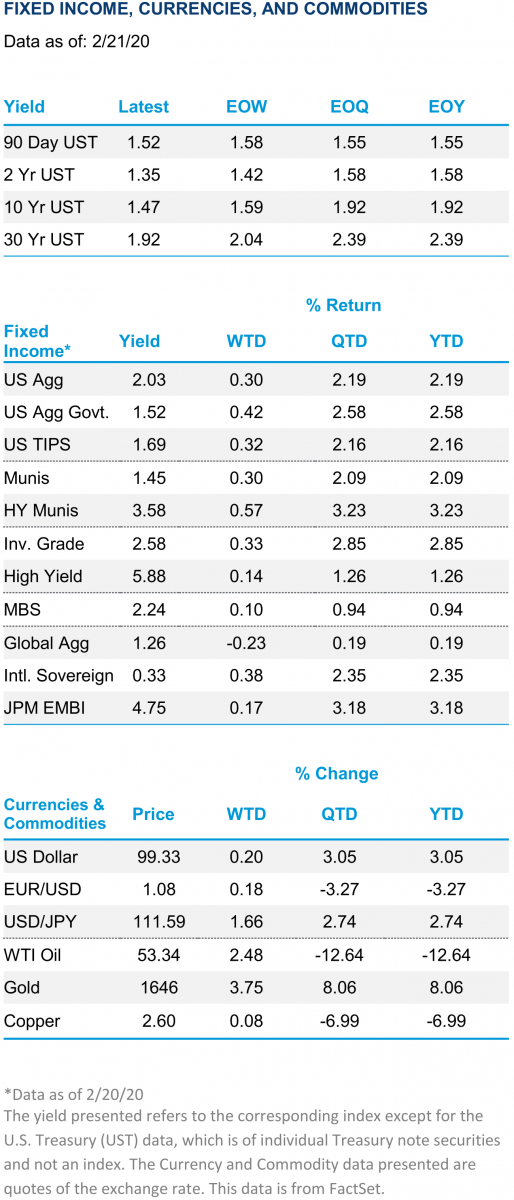

Fixed Income, Currencies, and Commodities

Fixed income prices were mostly up during the week as fears over the COVID-19 outbreak and related economic uncertainty drove yields down. The 10-year U.S. Treasury yield fell 12 basis points (0.12%) as the yield curve flattened and the 3-month/10-year spread slipped back slightly into inversion territory. The 30-year Treasury yield hit a record low of 1.89% Friday morning before rising slightly during the session. High-yield municipal bonds posted the best return through Thursday, finishing up 0.57%. The only index that we track to post a loss was broad international core bonds, which ended down 0.23%.

Oil was up for six straight sessions through Thursday before falling slightly in Friday’s trading to end the week up. Gold finished the week strongly to end at its highest levels in seven years as investors looked to safe haven assets. The U.S. dollar posted its sixth weekly gain in the past seven weeks, helped by strong performance against the Japanese yen following weak Japanese manufacturing and gross domestic product (GDP) data over the past week.

Next week’s U.S. economic calendar includes consumer confidence reports from the Conference Board and University of Michigan; new and pending home sales; revised fourth quarter GDP; durable goods orders; and personal income, spending, and inflation data for January from the Bureau of Economic Analysis.

Earnings season continues next week with 41 S&P 500 companies slated to report quarterly results.

Internationally, the most important data to watch will be the PMI data coming out of China, where the impact from the COVID-19 outbreak is expected to be significant. The economic calendar in Germany includes GDP, business sentiment, and consumer inflation data. In Japan, data on retail sales, industrial production, and housing construction will be released.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

- References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

- U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

- All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

- For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

- This research material has been prepared by LPL Financial LLC.

- Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisorthat is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- If your advisor is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

- Tracking # 1-95452

Contact us directly should you have questions about this topic.