4.16.26 Tactical Positioning Update: From Preparation to Action

Over the past year, LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) has emphasized that tactical investing does not require constant activity. Instead, it requires preparation, patience, and the discipline to act only when the expected benefit of a change clearly outweighs the risks. We have made some changes to our Tactical Asset Allocation (TAA) guidance but continue to reflect that disciplined philosophy.

STAAC has updated our TAA to move portfolios to modestly overweight equities and underweight fixed income. Importantly, this adjustment builds on positioning decisions made well before volatility increased, rather than reacting to market stress after the fact. In our view, the recent increase in volatility has improved the prospective risk‑reward for taking incremental equity risk, allowing us to translate preparation into action while remaining within our established tactical framework.

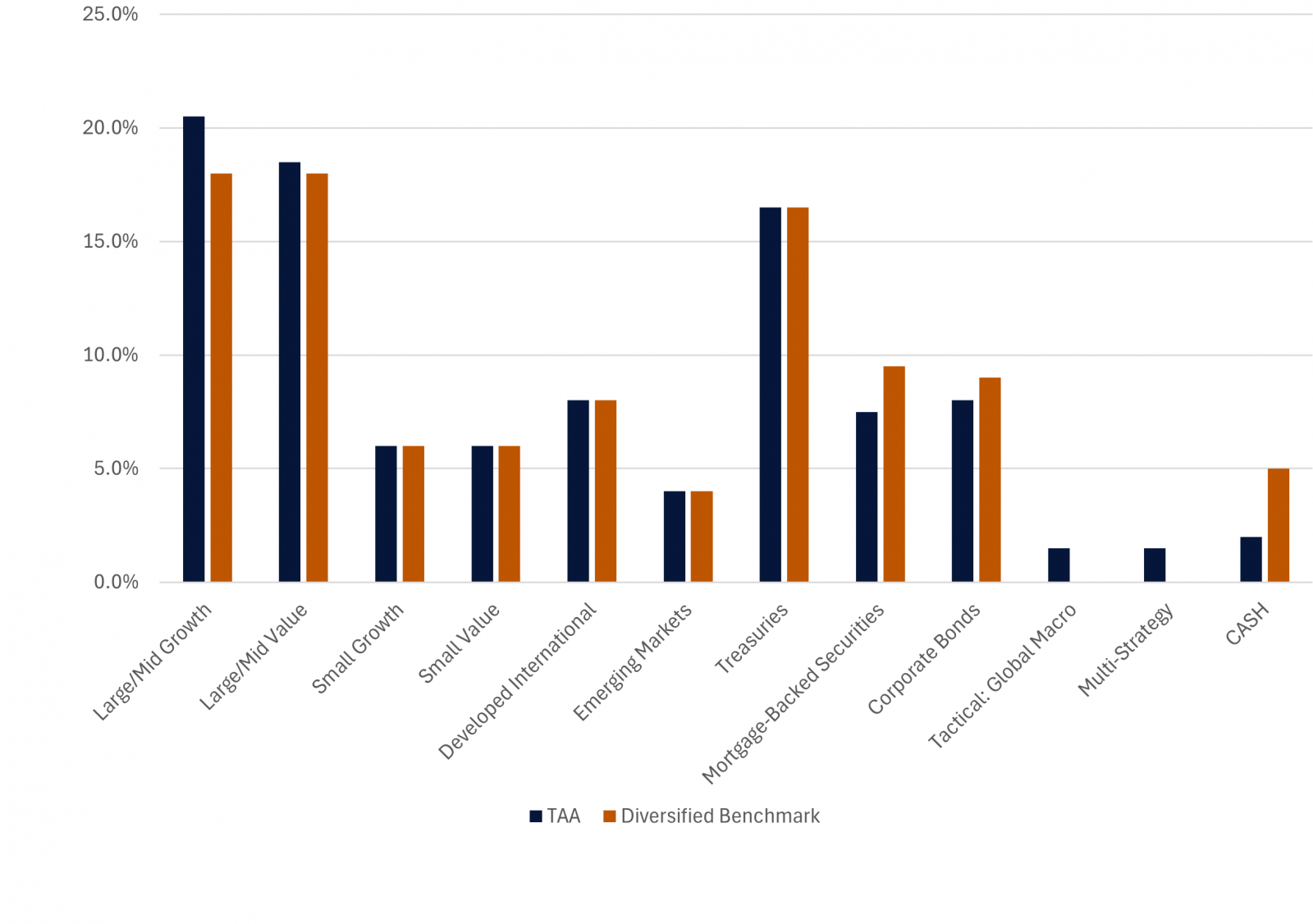

Our Growth with Income (GWI) portfolio, which tracks most closely the traditional 60/40 stocks/bonds portfolio, is shown below, and compared to our GWI Diversified benchmark.

LPL Research Growth with Income (GWI) Tactical Asset Allocation (TAA)

- Source: LPL Research 4/16/2026

- Disclosures: Past performance is no guarantee of future results.

What Changed?

The recent adjustment reflects two related allocation changes:

• Neutralizing the existing underweight to U.S. small cap value, which results in a modest equity overweight

• Reducing exposure to mortgage‑backed securities to fund that change

From a portfolio construction perspective, this shifts the Growth with Income model slightly above benchmark equity exposure while keeping overall portfolio risk well within the intended tactical range. The adjustment reflects an improvement in expected forward equity returns following recent market weakness, coupled with a more restrained outlook for select areas of core fixed income where valuations and technicals appear less supportive.

This is not a wholesale change in positioning or a reversal of longer standing views. Large cap equities and growth‑oriented exposures remain preferred within U.S. equities, and quality remains a central theme across asset classes. However, as dispersion has increased and valuations have reset modestly, we believe the relative opportunity set for equities has improved compared to mortgage‑backed securities.

Why Add Small Value Here?

Our upgrade of small value to neutral is primarily driven by our quantitative analysis work indicating durable technical trends that have developed since the start of the new year. With a path to ending the Iran conflict emerging and related lessening risk of extreme negative outcomes, we expect equities to broadly outperform fixed income. Fundamentally, small value stocks are supported by attractive valuations, bank deregulation, and robust capital investment. In an environment that is likely to get more supportive of risk-taking, eliminating the small cap underweight and moving to an overall overweight equities position seems prudent.

Why Reduce Mortgage-Backed Securities?

Our multi-year overweight position in MBS has served us well in terms of relative performance vs. the broad bond market. However, over that time, spreads have tightened meaningfully and remain below longer-term averages, diminishing the relative attractiveness of the asset class. While near-term momentum of lower interest rate volatility and constrained net supply may continue through the first half of the year, already tight spreads and the eventual likelihood that lower mortgage rates will increase prepayment risks may potentially cap returns.

What Are Our Other Tactical Views?

Following this update, our Tactical Asset Allocation reflects the following underlying themes:

• A slight overweight to equity risk expressed through domestic large cap growth

• An emphasis on balance sheet quality and earnings durability

• Continued caution in fixed income (MBS and Corporates) amid rate volatility and changing supply and demand dynamics

• A continued overweight to diversifying strategies / alternative investments, specifically multi-strategy and global macro strategies, funded from cash.

Why This Is Our First Tactical Trade of the Year

Coming into 2026, we made a deliberate and somewhat contrarian decision to position portfolios more defensively and with greater diversification than was broadly expected at the time. That decision was grounded in the view that market conditions were unusually complacent and that the range of potential outcomes was wider than reflected in asset prices. While that positioning ultimately proved to be early, it has been beneficial on a relative basis as volatility has increased and correlations have shifted.

That preparation matters. Because those diversification decisions were made earlier, we are not being forced to de‑risk or reposition under pressure today. Instead, we are able to evaluate opportunities from a position of strength, with the flexibility to adjust risk as expected forward returns improve. This trade reflects that dynamic. It represents a measured re‑engagement of equity risk when conditions became more favorable, rather than a reaction to recent price action.

Periods like this highlight the risks of being overly active. Tactical investing does not mean frequent trading. Highly reactive decision‑making in volatile environments can easily result in being whipsawed, such as reducing risk near market lows or adding it back after prices have already rebounded. It can also introduce unnecessary transaction costs and tax inefficiencies. We believe restraint, when warranted, is often the most effective expression of tactical discipline. Tactical does not mean frequent. It means nimble, but selective.

Final Thoughts

This TAA update reflects the progression of a disciplined process. Preparation came first. Patience followed. Action comes only when the expected benefits justify the risks. We will continue to monitor economic conditions, market developments, and technical signals closely. Volatility can be uncomfortable, but it is also what creates opportunities for investors who remain disciplined and avoid the urge to overreact.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #1093790