7.2.26 Weekly Market Performance

As market watchers prepared for America’s 250th birthday celebration, global equity markets delivered a strong finish to the second quarter. The S&P 500 printed its best quarterly return since 2020 amid high profile economic data and rotation dynamics, while also posting a moderate gain over the holiday-shortened week. Asian equities capped their best quarterly result since 2009 while European shares also sealed their best quarter in six years. Fixed income markets traded lower over the last four days after ending a positive quarter. In commodities and currencies, oil continued to fall and the yen remained on intervention watch.

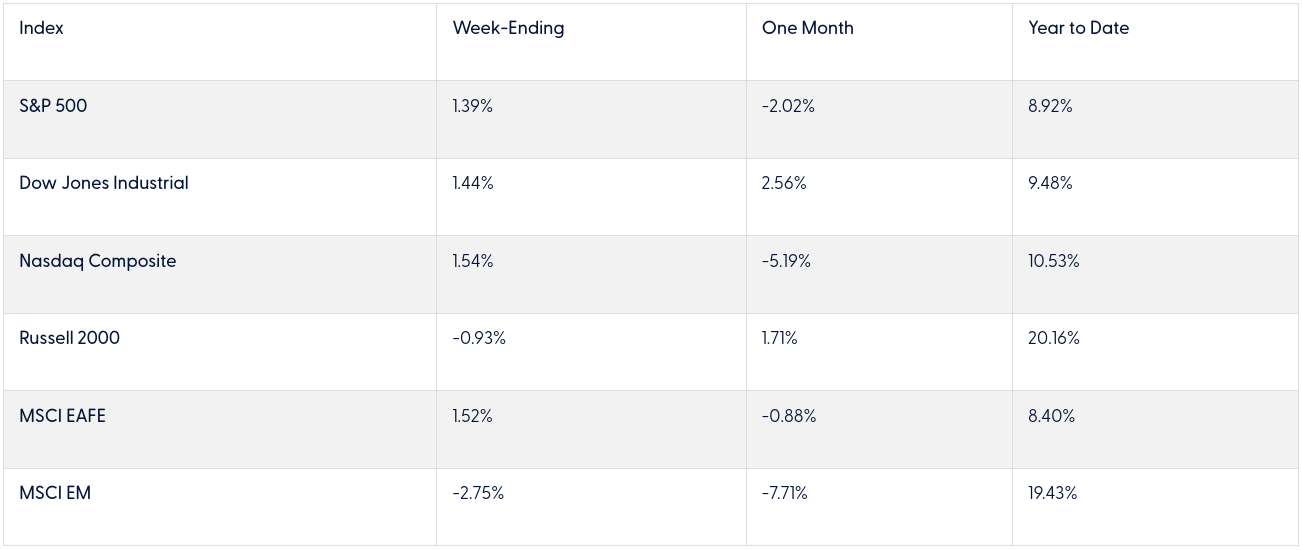

Stock Index Performance

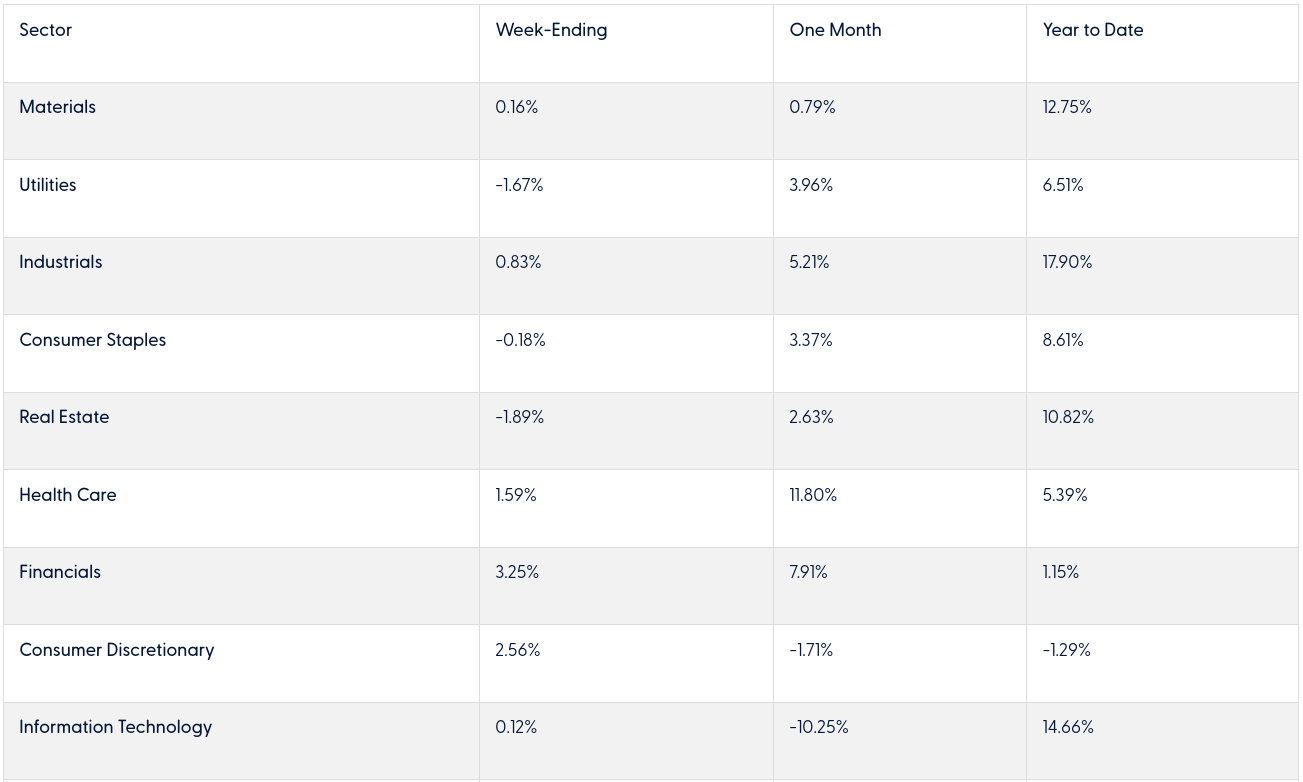

S&P 500 Index Sectors

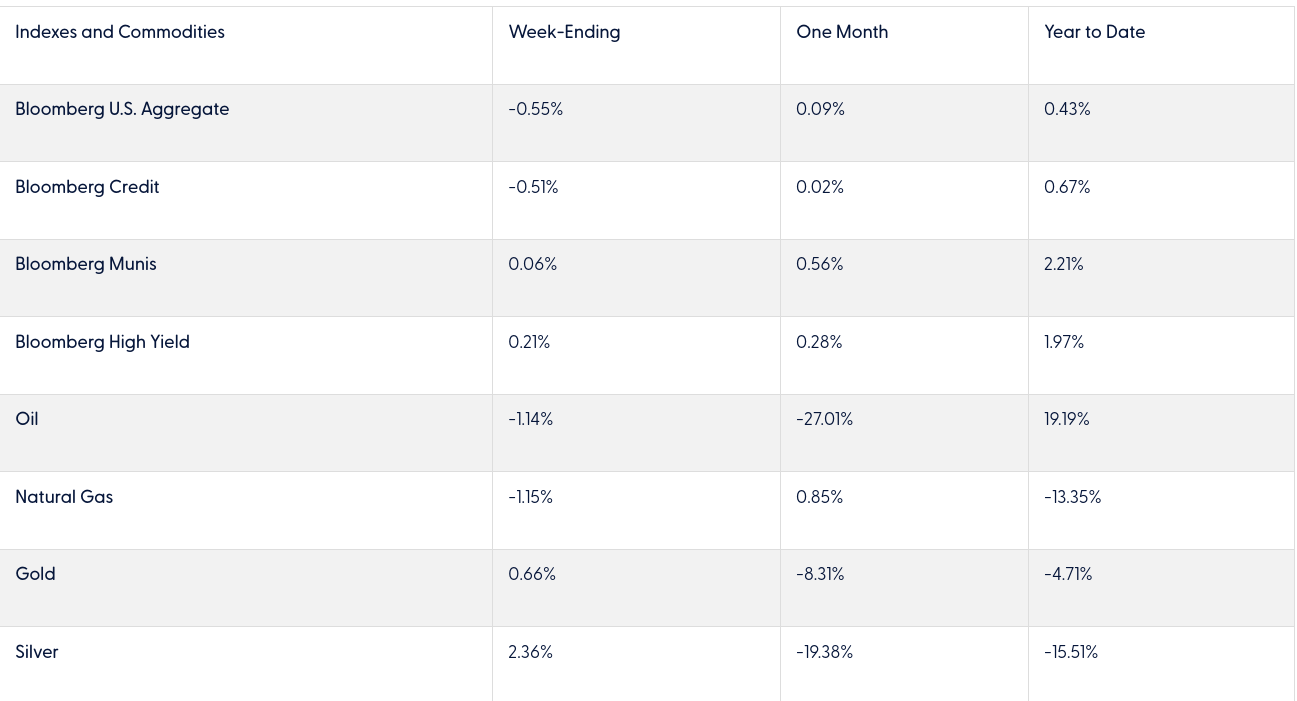

Fixed Income and Commodities

-

Source: LPL Research, Bloomberg 7/2/26 @ 3:10 p.m. ET

-

Disclosures: Indexes are unmanaged and cannot be invested in directly.

U.S. and International Equities

U.S. Equities: Stocks celebrated the 250th anniversary of the Declaration of Independence with solid gains this week after capping a blockbuster second quarter. Major averages rallied into quarter-end as dip buying emerged after last week’s slide, fueling a bounce in Magnificent Seven names further aided by macro data that generally underscored the resilient economic narrative. The S&P 500 sealed a 15.2% quarterly gain (including dividends) to mark its best quarter since 2020, while also capping a 10.2% total return over the first half of 2026.

Sentiment turned cautious to start the second half as investors appeared to book gains in semiconductor shares after the space logged its best quarterly advance on record. Breadth remained positive under the surface, however, with software, select Magnificent Seven names, and other recent underperformers faring well amid a continuation of momentum unwinding and rotation dynamics. Most S&P 500 constituents continued to rise despite chipmakers dragging on major indexes Thursday as bad news appeared to be good news for Wall Steet after weaker-than-expected payrolls data threw cold water on near-term rate hike expectations.

International Equities: European stocks tracked a healthy weekly advance on the back of Thursday’s rally. The region capped its best quarter since 2020 on Tuesday with the STOXX 600 Index ending June at record highs. Stocks were supported by European Central Bank (ECB) President Lagarde remarking that Europe is becoming less vulnerable to economic shocks on the final session of the quarter and shook off some hawkish-tilted central banker remarks during the following session to bounce back strongly as bets of a U.S. rate hike faded. Germany’s DAX Index led the late week rally, further supported by government officials unveiling an $11.4 billion annual tax relief package and a range of measures aimed at supporting the labor market.

Asian equities were on pace for a mostly lower week through Thursday’s session. Most major markets pared week-to-date gains following Thursday’s drop, with South Korea wiping out early week AI spending plan-driven gains as the National Pension Service resumed rebalancing and chipmakers faced downside pressure. Taiwan was a relative outperformer, alongside Hong Kong, which received some support from oversold technical indicators. Nonetheless, at Tuesday’s quarter-end the Asia-Pacific region sealed its strongest quarter since 2009, highlighted by Korea’s best quarterly result since 1998 and the strongest on record for Japan’s Nikkei.

Fixed Income, Currency, and Commodity Markets

Fixed Income: Core bonds, as measured by the Bloomberg Aggregate Index (Agg), traded lower on the week, weighed down by a notable mid-week rise in Treasury yields. Tuesday’s selling was triggered by a stronger-than-expected JOLTs jobs report, accelerating through the afternoon on likely month-end related flows before paring losses slightly on Thursday. Treasuries traded mixed on Thursday as Fed rate hike expectations ebbed, bolstering shorter-dated securities after softer than expected June payrolls data arrived less than one day after Fed Chair Kevin Warsh stated that price pressures have eased.

Earlier in the week, the Treasury market posted a slight monthly gain for June with support stemming from falling crude oil prices, partially offset by last month’s decidedly hawkish Fed meeting and strong economic data. Bond market sentiment was also shaped by a strong month for equities and record corporate bond issuance. For the quarter, the Agg bounced off mid-May lows to add 0.7%, while corporate bonds outperformed with a 1.4% return while mortgage-backed securities lagged with just a 0.6% advance.

Commodities and Currencies: The broader commodity complex was little changed through Thursday afternoon. Energy commodities dropped over the last four days, although losses were relatively modest, including roughly 1% losses for crude oil and natural gas prices. Last week’s declines for West Texas Intermediate (WTI) crude oil spilled over into the new week, hovering near pre-war levels on continued hopes that the mild recovery in traffic through the Strait of Hormuz is a precursor to returning to pre-conflict trends. Among highlights in the Persian Gulf, the United Arab Emirates reportedly restored its exports to over 3.9 million barrels daily. Easing concerns of a return to kinetic conflict also pressured crude prices. In metals, gold traded modestly higher, supported by reduced rate hike expectations following soft payrolls data and Fed Chair Warsh’s remarks of easing price pressures. Meanwhile, the U.S. Dollar Index dropped Thursday after hovering near the flatline on the same dynamic, although the yen remained in the currency spotlight. Price action was jittery for the Japanese currency as traders closely watched for signs of intervention from Tokyo as stubborn weakness near 40-year lows persisted.

Economic Weekly Roundup

Highlights from Friday’s Payrolls Release:

• Friday’s Bureau of Labor Statistics report showed that an additional 2.5 million have dropped out of the labor force since last year.

• Payrolls grew by 57,000 in June, supported by gains in business services and health care. The Leisure and Hospitality sector lost jobs.

• Those not in the labor force rose by roughly 2.5 million to 105.8 million, most likely due to folks giving up looking for work.

• The unemployment rate ticked down to 4.2% as fewer people were looking for a job last month. In a strong economy, a low unemployment rate can coexist with healthy participation rates but that’s not the case now.

• Hours worked declined, indicating an upcoming slowdown in broader economic activity.

• Flows are revealing and provide another perspective on the labor market. We’ve seen a rising trend in people dropping out of the labor force (whether they were previously employed or unemployed). This suggests the job market is cooling down.

Bottom Line: Firms are still adding to their payrolls, but hours worked are below pre-pandemic levels as firms cut back labor utilization. A concerning trend is the increasing flow of individuals dropping out of the job market altogether. For now, the labor market is holding, giving the Fed opportunity to stay focused on price stability.

The Week Ahead

The following economic data is slated for the week ahead:

• Monday: S&P Global U.S. Services and Composite PMIs (Jun final), ISM Services Index (Jun)

• Tuesday: ADP Weekly Employment Change (Jun 20), Trade Balance (May)

• Wednesday: MBA Mortgage Applications (Jun 3), Wholesale Inventories (May final), FOMC Meeting Minutes (Jun 17), Consumer Credit (May)

• Thursday: Initial Jobless Claims (Jul 4), Continuing Claims (Jun 27), Existing Home Sales (Jun)

• Friday: No economic releases scheduled

- Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

For Public Use – Tracking: #1135002